SUMMARY

- U.S. Equities: I remain slightly bullish on U.S. equities. I am maintaining a patient approach by focusing on high quality, growing companies rather than aggressively adding to risk at current valuations. Investors should closely monitor whether the Iranian conflict and high oil prices begin to erode strong earnings forecasts or if the major indices break below their critical 200-day moving average support levels. I view the current volatility as a potential opportunity to increase risk exposure if the market takes another material leg lower and reaches more attractive valuation thresholds.

- International Equities: I am maintaining a slightly bullish outlook on international equities with a preference for high-quality companies across developed and emerging markets while waiting for more attractive valuations. Although a swift resolution to the Iranian conflict could trigger a significant relief rally and create long-term opportunities, like in the U.S., current uncertainty makes the 200-day moving average a critical technical threshold to watch across international equity indices.

- High Income-Generating Assets: I remain moderately bullish on high-income assets like credit-sensitive bonds and dividend stocks, as their absolute yields are compelling and they can potentially act as a lower-volatility complement to equities. While credit spreads are currently tight and have room to widen if geopolitical tensions escalate, these assets provide a strategic source of “drier powder” and reliable cash flow generation while I wait for better equity entry points.

- Commodities (Gold & Oil): I have a mixed outlook on commodities. I moved to a moderately bearish stance on WTI Crude Oil after its recent spike to nearly $120 per barrel with the potential for the Iran conflict to ease in the coming months. I am fundamentally cautious on gold but remain technically bullish because the price continues to hold above key 50-day and 200-day moving averages despite a rallying U.S. dollar.

- Conservative Assets (Bonds): I remain slightly bullish on bonds to try to seek some diversification relative to equities in the current volatile environment. Credit spreads remain tight, and taking aggressive credit risk doesn’t make sense to me at the moment. I prefer to remain diversified across bond sectors, credit quality, and duration through exposure to active bond managers.

- Other (Hedges): I remain slightly bullish on non-traditional hedging but prefer to keep it simple by using credit-sensitive bonds and high-income assets to manage current equity volatility. I am staying patient and letting the market come to me, ready to tactically rebalance or add risk only if prices decline to more attractive valuation levels.

The current geopolitical friction involving the U.S., Israel, and Iran serves as a stark reminder that external shocks are a permanent fixture of the investing landscape. While the Trump administration has stated that these targeted strikes will conclude within a month or two, seasoned investors know that actions always carry more weight than verbal assurances.

We have observed a recent spike in the S&P 500 Volatility Index. Even with this increase, the VIX remains well below the extreme levels seen during the Liberation Day events of last spring. This historical context illustrates that while markets are uneasy, we are far from a state of true panic.

S&P 500 Volatility Index

Energy markets are feeling the most direct fundamental impact of this conflict. WTI Crude Oil recently surged toward $120 per barrel before retracing to the $100 level. This price action creates two distinct paths for the global economy. If the conflict resolves quickly as the administration predicts, we could see a massive reduction in geopolitical risk. This scenario could spark a bullish reversal as oil prices stabilize and risk appetite returns to the market.

WTI Crude Oil

Conversely, if the struggle drags on and oil remains significantly higher, the outlook could turn weaker. Persistent high energy costs could force investors to lower their expectations for corporate earnings and broader economic growth and equity markets could decline further. Then, from a technical analysis perspective, if equity price trends turn negative and lead to broken support levels, equity markets could quickly move another leg lower.

Speculating on the exact duration of military conflict is a futile exercise because the variables are impossible to forecast consistently. A single positive announcement regarding diplomatic discussions could flip market sentiment from bearish to bullish in minutes. The Trump administration’s insistence that this will not be a prolonged war is currently providing a soft floor for asset prices. Rather than guessing on headlines, I prefer to let the markets come to me by focusing on high quality assets with strong fundamentals and tactically increase risk when prices are at levels I deem attractive enough.

Before this recent volatility, U.S. large cap valuations were extended and credit spreads were notably tight. Those conditions signaled a time for me to take a more risk neutral posture. Now that risk assets are beginning to sell off, we may get opportunities to take advantage of short-term dislocations in the market. I am beginning to look for tactical rebalancing opportunities in areas that have sold off more materially than others, yet I see no reason to aggressively increase overall risk at these levels. The current environment just doesn’t offer enough of a “fat pitch” for me to swing at and add risk to my investments.

As I always try to do, I’ll continue to remain patient and let the markets come to me.

While the conflict in Iran is dominating the headlines, other factors have implications for the broader global economy and corporate earnings growth.

The Shifting Landscape of U.S. Trade Policy

On February 20, 2026, the U.S. Supreme Court delivered a landmark 6 to 3 decision to strike down the sweeping global tariffs that the Trump administration had implemented under the International Emergency Economic Powers Act. The ruling clarified that this specific emergency statute does not grant the executive branch the authority to unilaterally impose taxes on imports. This decision fundamentally invalidated billions of dollars in collected duties and provided a sudden flash of relief for U.S. importers and consumers who typically bear the brunt of these costs.

Businesses generally dislike uncertainty, and the actual impact of the Court’s decision remains unclear. It is yet to be determined if companies will receive full refunds or if the administration will find alternative legal avenues to reimplement the tariffs. Until these questions are answered, business activity and capital investment may remain constrained.

Sticky Inflation and the Federal Reserve

Inflation continues to remain somewhat sticky in the 2.5% to 3.5% range. The Federal Reserve primarily monitors Core PCE, which measures personal consumption expenditures while excluding volatile food and energy prices. If the conflict in Iran continues to disrupt oil prices and starts to negatively impact the broader U.S. economy, the Fed may be forced into a difficult position. They might choose to look past higher energy costs to determine if lower interest rates are necessary to support a slowing economy.

Given current inflation levels, the Fed may not feel a sense of urgency to aggressively reduce the fed funds rate. This remains true despite President Trump’s recent nomination of Kevin Warsh to replace Jerome Powell as Fed Chairman. Warsh is historically known for a more hawkish stance on inflation, though he has recently discussed how productivity gains from artificial intelligence could allow for lower rates.

Looking Toward the Mid-Term Elections

Early indications and generic ballot polls suggest that Democrats have a credible path to taking leadership in the House of Representatives. The Senate remains highly competitive and is still very much up for grabs. Much of this political outlook is already known and may already be priced in by the financial markets. If these early estimates remain steady, the eventual election results may not trigger significant market volatility. If we begin to see a definitive shift where Democrats appear likely to take a majority in both chambers, markets could react quickly as they attempt to price in a potential new legislative and regulatory environment.

My Positioning and Tactical Adjustments

Even with the recent conflict in Iran and the resulting surge in volatility, my views and approach haven’t changed. I am staying patient and letting the financial markets come to me. I have no interest in speculating on the exact date this conflict will end. If global equity prices and credit spreads reach levels that I find attractive, I will increase risk exposure at that time. Until then, I’ll continue to focus on tactical rebalancing when and where it makes sense to do so. In this environment, I still prefer to be diversified in higher quality, growing companies across market cap and geography.

Even before the situation in Iran escalated, U.S. mega-cap technology companies and speculative artificial intelligence stocks had begun to falter. I have previously expressed concern regarding extended valuations and the speculative fervor in these areas. Seeing these areas lose momentum is actually a constructive development for the long-term health of the market, in my opinion. I much prefer a market driven by earnings and fundamental value rather than one fueled by pure speculation and momentum.

Other areas where I have maintained a more favorable outlook, particularly in higher quality mid and small companies in the U.S. and broader exposure in developed and emerging international markets, performed well over the last few months. Unfortunately, these areas have declined quickly as volatility has picked up recently. While valuations in these areas were becoming slightly stretched, the recent sell-off has brought them much closer to their historical normal ranges. Still, valuations are still not as compelling as they were at the start of last year before the major rally. For this reason, I don’t have a need to aggressively increase risk at these current levels.

I continue to favor exposure to multi-asset income strategies, which have shown some resilience and performed well recently. As investors rotate out of expensive, tech-heavy names and into traditional value stocks and dividend-paying companies, these income-focused strategies have benefited. I plan to maintain a diversified exposure to these high income-generating assets and strategies for the foreseeable future.

Slight Deleveraging of Leveraged Exposure

I haven’t had any significant movement in the tactical strategies that I manage this year, except for a slight risk reduction in my U.S. Core X strategy.

In the U.S. Core X strategy, I executed a minor reduction in risk by trimming my mid-cap equity position. Throughout 2025, mid-caps generally lagged behind both large-cap and small-cap stocks. As mid-caps rallied to start 2026, they finally reached my predetermined price target, so on January 6, I reduced my leveraged exposure to U.S. mid-caps. This move brought my leveraged position back to a neutral stance, and I have maintained that positioning since. While the broader market has been volatile, this adjustment was based on pre-determined price target, not based on any shifts in my fundamental views.

I have not made any tactical adjustments to my Global Unconstrained strategy since my last update. I continue to hold a diversified mix of U.S. and international equities across market cap and investment styles. Within the high income space, I still favor multi-asset strategies but remain underweight on closed-end funds. This caution is due to credit spreads and closed-end fund discounts to net asset value remaining tight, which creates enough potential downside risk I’m not willing to take at these levels.

Despite the recent elevated market volatility, I am maintaining leveraged exposure to specific areas where I continue to see upside potential. This includes U.S. biotech, mid-caps, small-caps, diversified emerging markets, and Chinese equities.

If volatility continues to climb and areas of the market experience a more significant decline, I have sufficient liquidity to increase risk exposure. Until those opportunities present themselves, I will remain patient and let the markets come to me.

RISK ASSETS

Market Outlook: Navigating Volatility Through Quality and Yield

I maintain a slightly bullish stance on risk assets at this time. Although we have witnessed a recent market selloff, the current declines are not severe enough for me to justify a significant increase in overall risk exposure. My core investment thesis remains unchanged over the last few months. I continue to prefer broad diversification focused on high quality growing companies complemented with income generation across asset classes and income strategies.

We have seen a stalling or significant selling off in mega-cap technology and speculative artificial intelligence stocks, which I think is a healthy development for the broader market. These areas, along with unprofitable momentum stocks, had reached valuations that caused me concern. I think their deeper correction might allow for a more sustainable market structure. Outside of these areas, high quality mid and small cap stocks have performed relatively well. I think this is at least somewhat encouraging as valuations don’t appear as extended and quality fundamentals continue to offer support. While some speculative pockets had been re-emerging in the small cap space, I continue to prefer diversification into higher quality mid and small cap companies.

International Markets and Macroeconomic Headwinds

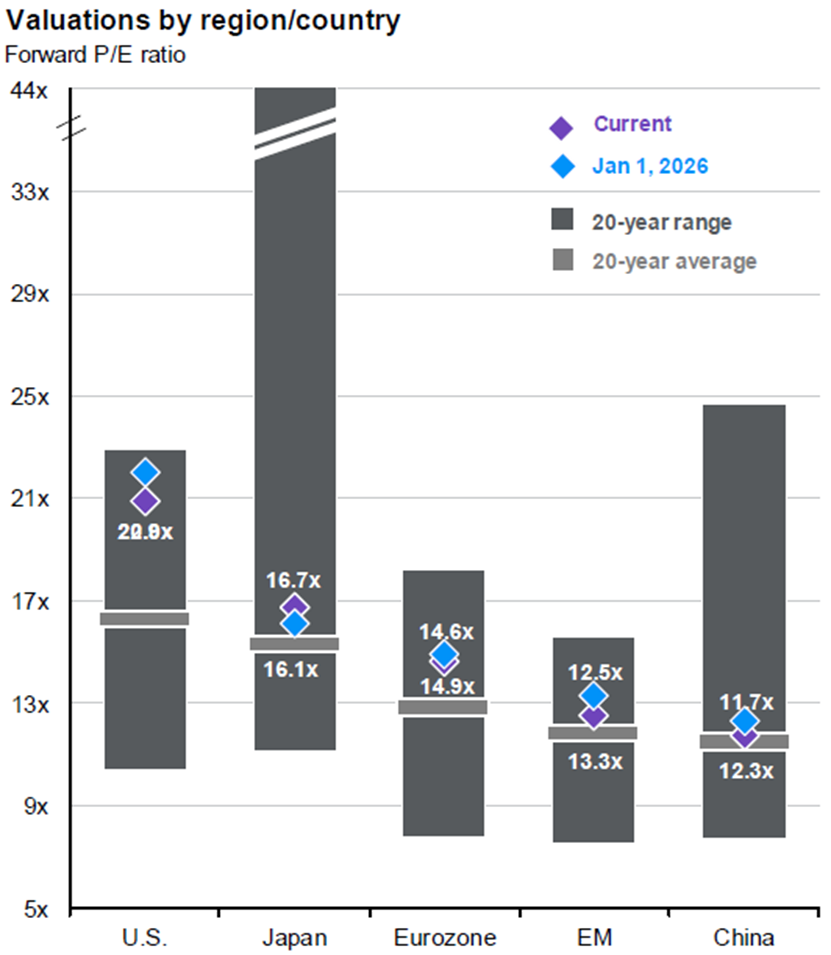

I think international developed and emerging markets still offer growth potential and valuations appear to be more attractive than comparative U.S. equities, even if that gap has narrowed since early last year.

With the conflict in Iran pushing oil prices higher, investors should remain cognizant on their impact to companies and consumers energy costs. Higher oil prices could disproportionately hurt foreign markets, especially in Europe, while the U.S. remains a relatively strong domestic producer. In this environment, I continue to prefer diversified exposure to higher quality, growing companies that can navigate economic pressures over the longer term.

The Income Advantage and Private Credit Risks

Investors can still find attractive yields in income-generating strategies, including option income strategies, credit-sensitive bonds, and closed end funds. Income yields in the range of 6% to 8% could be attainable and offer a potential defensive cushion compared to the volatility of pure equity market exposure.

I continue to like credit-sensitive bonds as a lower-volatility complement to stocks. While I also like high quality dividend growers for the longer-term, volatility in the short term could elevate from here. I am staying relatively cautious with closed end funds. These funds often use leverage which naturally increases price volatility. Since I’m seeing average discount to net asset values fairly tight, broadly speaking, being overly aggressive in this space does not make sense to me yet. I would wait for those discounts to widen significantly during a deeper market decline before adding more risk.

We are also beginning to see potential cracks in the private credit market. Investors are withdrawing capital from semi-liquid strategies in large volumes, forcing some prominent managers to halt redemptions. This creates a cycle of fear that can lead to a rush for the exits. Even if the underlying loans are fundamentally sound, a liquidity crunch might force managers to sell assets at fire sale prices to meet withdrawal demands. This is a critical area to monitor as it could signal broader stress in the financial system.

U.S. EQUITIES

I remain slightly bullish on U.S. equities at this time. My primary objective is to maintain a diversified stance by holding high-quality growing companies across all market capitalizations, sectors, and investment styles, including growth, core, and value.

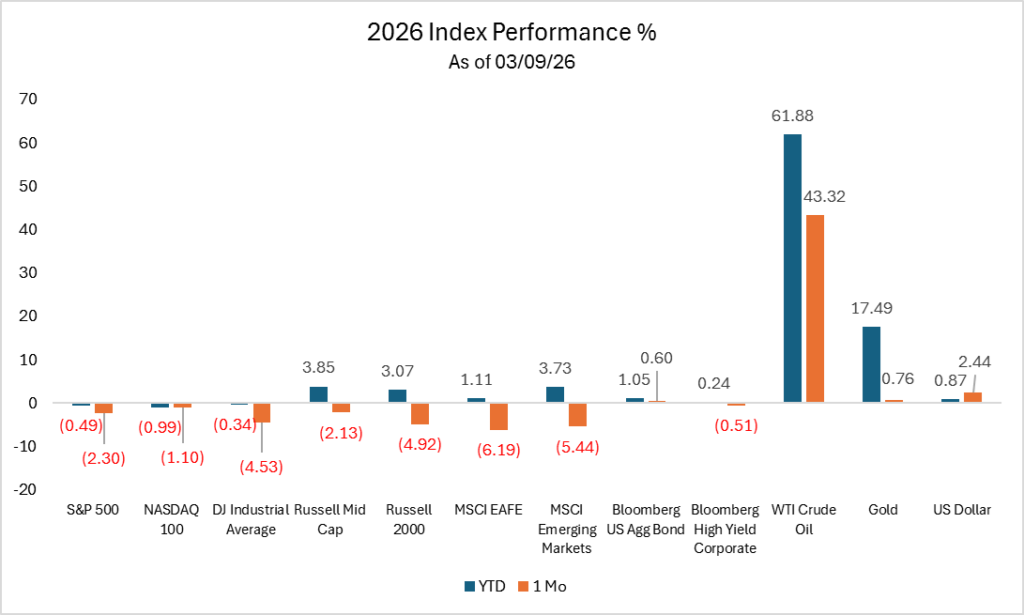

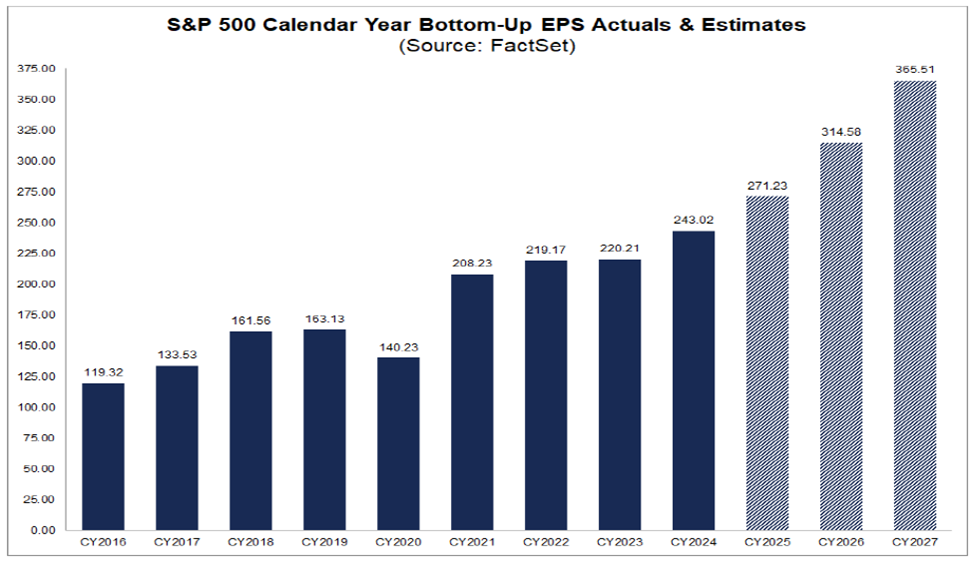

Recent data from FactSet indicates that analysts anticipate strong earnings growth for the S&P 500 Index through 2026 and 2027. It is important to note that these optimistic projections were largely formulated before the recent conflict in Iran and the subsequent spike in oil prices.

If the Iran conflict resolves within the next month or two without causing significant damage to economic stability or corporate profits, investors may refocus on these positive fundamental forecasts. If a prolonged conflict keeps oil prices elevated and weakens consumer sentiment, that could necessitate a downward shift in expectations. In this scenario, financial markets could have a significant negative adjustment to reflect the diminished growth outlook.

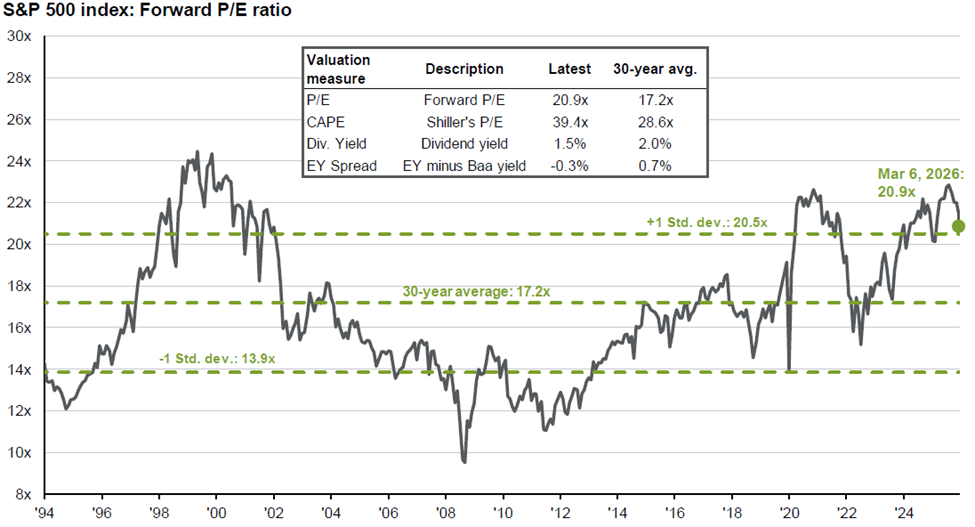

Valuations for the S&P 500 remain elevated, which leaves room for further downside price pressures to get to more normalized valuation levels. At these current valuations, it doesn’t provide a strong enough incentive for me to be overly aggressive in U.S. large-cap stocks, particularly at the S&P 500 Index and NASDAQ 100 Index levels. As a long-term investor, I prefer to stay disciplined and maintain broad exposure to growing, quality companies across the market cap spectrum. If the equity markets experience another material leg lower, I may consider that an opportunity to increase my overall U.S. equity exposure.

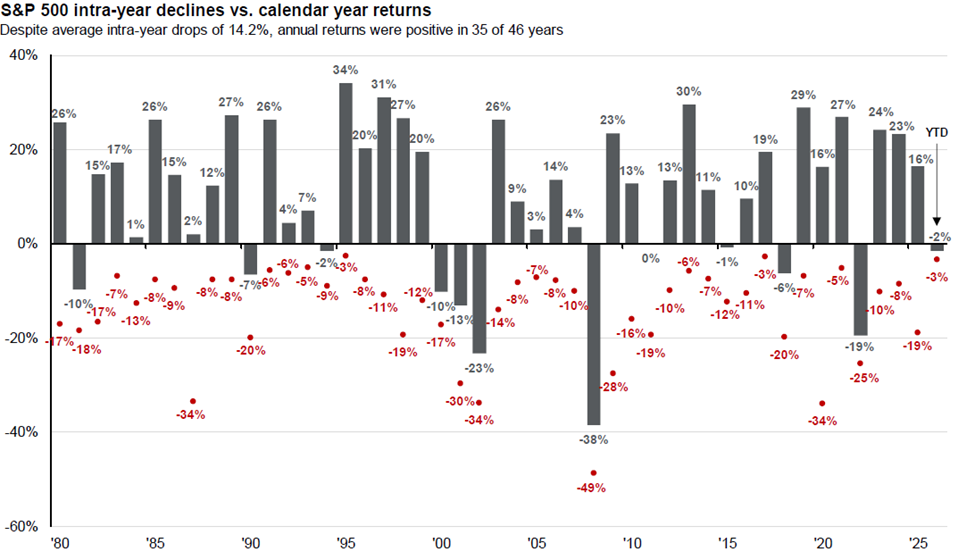

It’s always helpful to put short-term market volatility into a historical perspective. Historical data in the chart below shows that the S&P 500 Index frequently experiences annual peak-to-trough declines of 10% or more, even during years that ultimately end with positive total returns. Understanding this pattern can help set realistic expectations for future market pullbacks and reinforce the importance of staying the course during periods of stress.

Need to Pay More Attention to Market Technicals in This Environment

When external events like large foreign military conflicts impact financial markets, forecasting becomes incredibly difficult. In these moments, intermediate and long-term fundamentals often take a back seat to investor emotions and short-term momentum. In this type of environment, market technicals become more critical in determining the potential direction of prices.

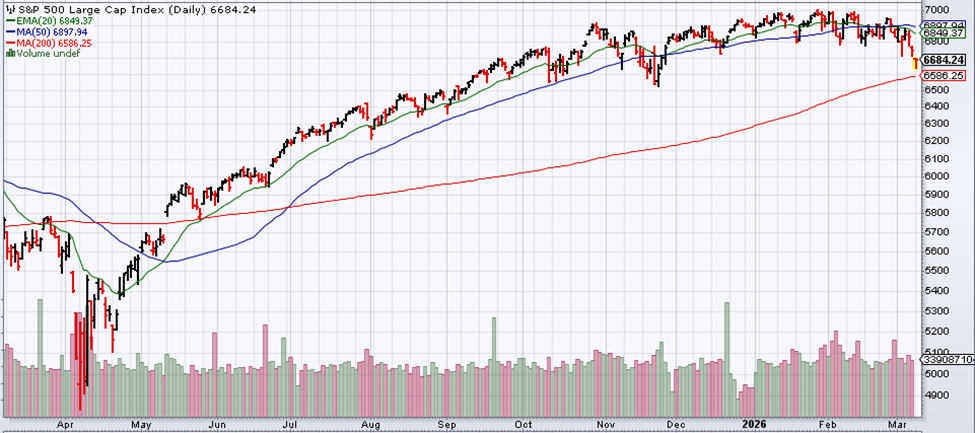

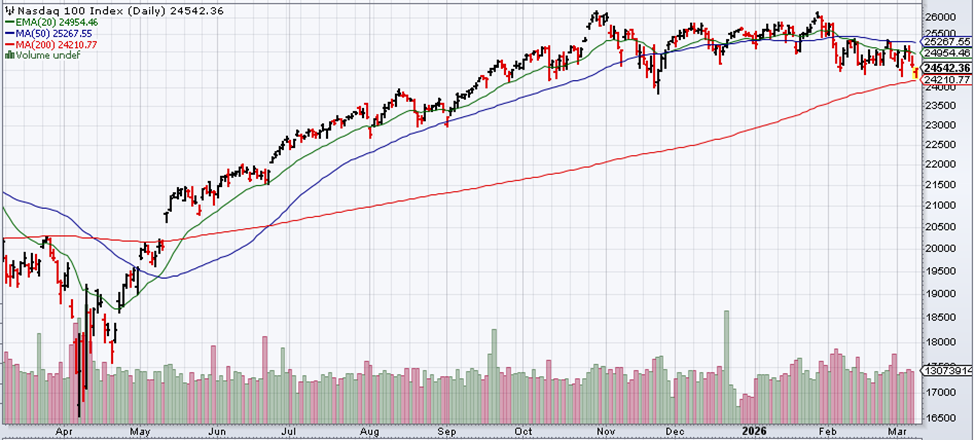

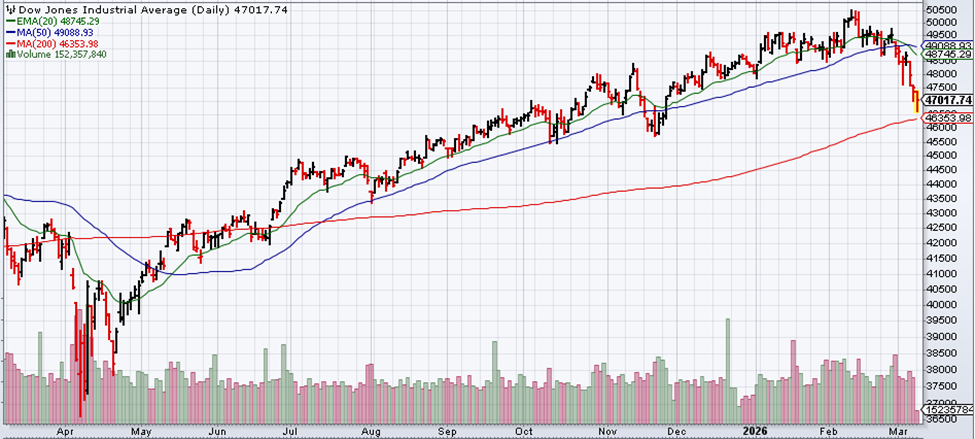

Currently, the major equity indices including the S&P 500, NASDAQ 100, and Dow Jones Industrial Average have fallen below their 50-day moving averages. Traders have now shifted their focus to the 200-day moving average as the next potential level of support. As of March 9, 2026, these indices are still holding above these long-term trend lines. If they were to decline below the 200-day moving average, volatility could spike and markets could quickly take another leg lower.

It’s important to remember that market technicals do not always correlate with long-term fundamentals. If enough capital follows these technical indicators, the market can move based on these “squiggly lines” regardless of the underlying fundamentals. This self-fulfilling prophecy can be a key driver in high-volatility environments where headlines dominate the narrative.

Unless we see a bullish development regarding the Iranian conflict, I would not be surprised to see the markets test and potentially fall below the 200-day moving average. If a quick drop occurs and volatility picks up significantly, I would consider adding to my equity risk exposure at those lower levels.

For now, I am remaining patient and letting the market come to me, as I am fully aware that technical weakness can drive prices lower in the short term despite the longer-term outlook.

S&P 500 Index

NASDAQ 100 Index

Dow Jones Industrial Average Index

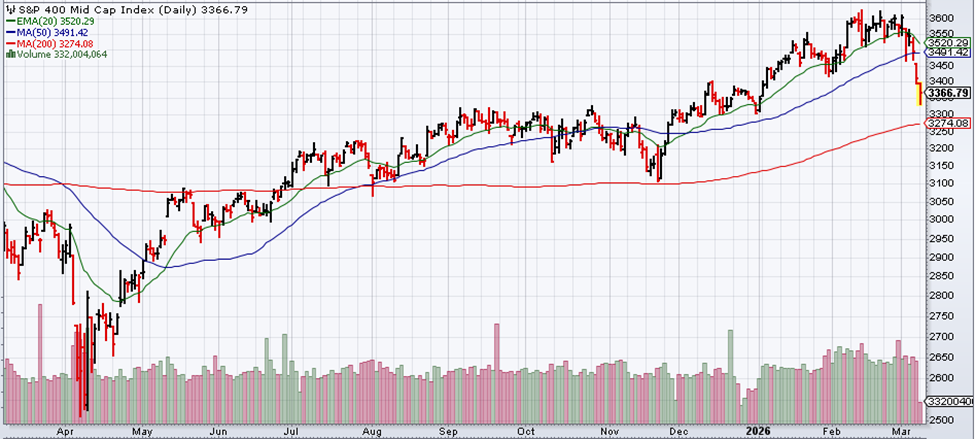

S&P 400 Mid Cap Index

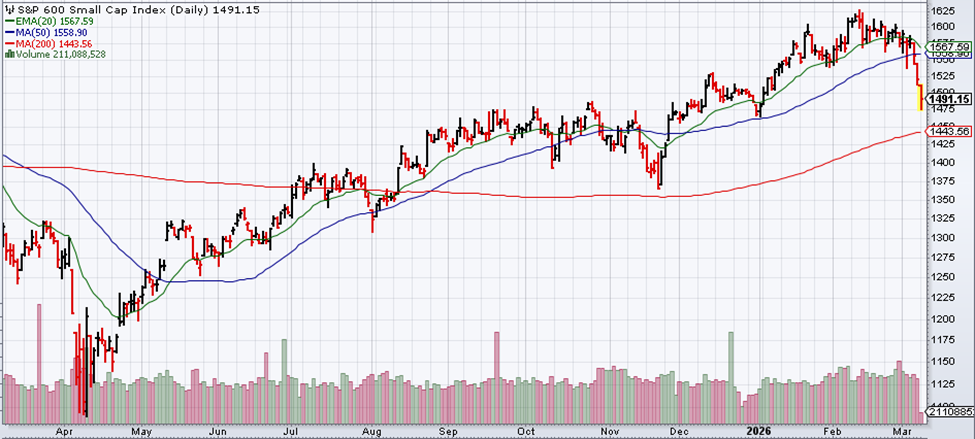

S&P 600 Small Cap Index

FOREIGN EQUITIES

I remain slightly bullish on foreign equities at this time. My preference is to stay allocated to high-quality growing companies across geographies, market cap, and investment styles (growth, core, value).

In my previous outlook, I reduced my stance from moderately bullish to slightly bullish following the significant rally in international developed and emerging markets throughout 2025. Despite the recent volatility and downward pressure on international stocks, I am maintaining this slightly bullish view rather than increasing my view to moderately bullish.

The onset of the conflict in Iran has caused valuations in international equity markets to come down a bit. It’s important to recognize that these valuations were coming down from somewhat elevated levels reached during the late 2025 surge. While current valuations are lower than they were just a few months ago, they have not yet reached levels that I would consider overly attractive.

Like with my views on U.S. equities, I’m remaining patient and will let the markets come to me.

If the current conflict in Iran is resolved quickly and geopolitical risks in the Middle East subside through a potential disarmament, international markets could see a powerful relief rally. If Middle Eastern geopolitical risks are drastically reduced for a sustainable, multi-year period, European and Asian developed and emerging markets may actually embark on a stronger growth path than previously anticipated. This could potentially provide a significant tailwind for international equities.

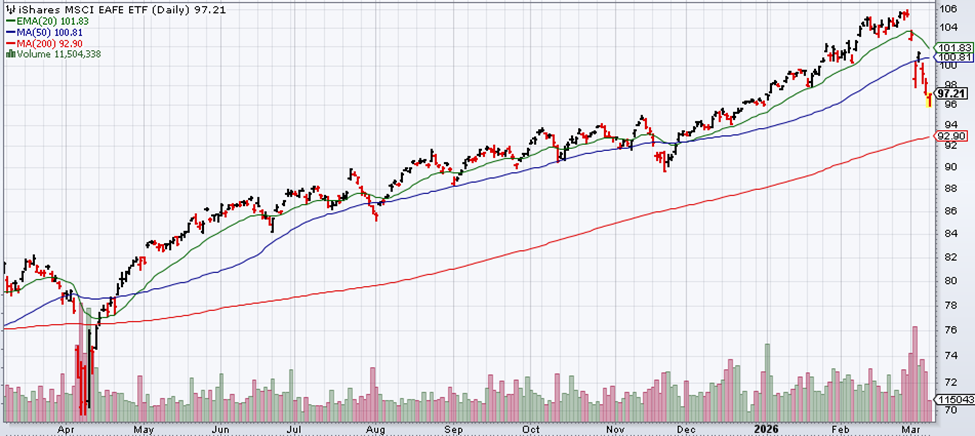

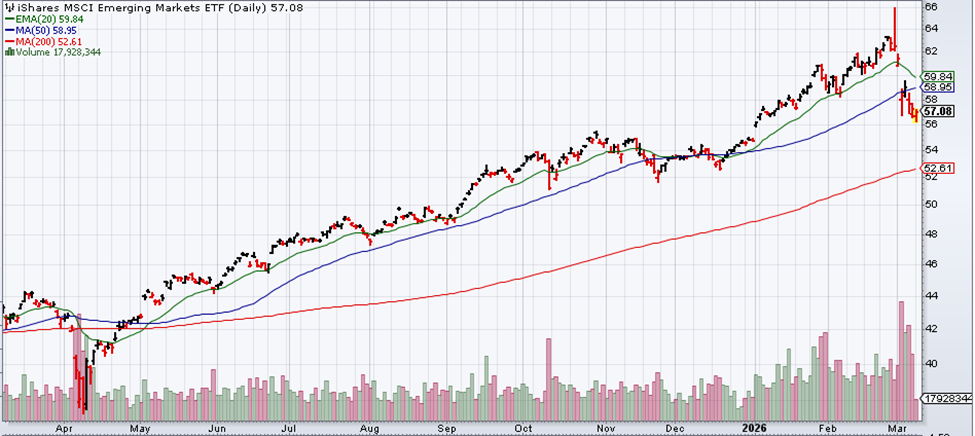

While that is a hopeful scenario, the current uncertainty and its ripple effects on the global economy requires market technical analysis to help serve as secondary guide for potential investment price direction. Currently, the MSCI EAFE Index (representing developed markets) and the MSCI Emerging Markets Index are both trading above their respective 200-day moving averages. These indices still have some cushion before hitting those long-term support levels, which remain the critical threshold for technical traders. If support is broken, we could see another leg lower in international equities.

MSCI EAFE Index (proxied by the iShares MSCI EAFE ETF)

MSCI Emerging Markets (proxied by the iShares MSCI Emerging Markets ETF)

U.S. Dollar

The U.S. Dollar Index has solidified its role as a premier safe-haven asset amid the ongoing Iranian conflict. The index has rallied close to the 100 level as investors flee riskier assets in favor of the perceived stability provided by the dollar. From a market technicals perspective, the dollar could remain within a defined trading range, with 100 acting as the upper resistance and 95 serving as the primary support on the downside.

The trajectory of the dollar could be heavily dependent on the duration and intensity of the Middle East conflict. If military operations in Iran escalate or result in prolonged disruptions to global energy supplies, we could see a decisive breakout above the 100 level.

If the conflict reaches a swift diplomatic resolution and geopolitical risks decline, the premium currently baked into the dollar could evaporate. In that scenario, the index could break below the 95 support level as capital rotates back into international developed and emerging markets.

This relationship makes the U.S. dollar a potential barometer of fear that investors should watch to gauge when the market might be ready to pivot back toward a risk-on environment.

U.S. Dollar Index

HIGH INCOME

I remain moderately bullish on high-income asset classes and strategies.

I consider credit-sensitive bonds, dividend-paying stocks, option income strategies, real estate, and closed-end funds as essential complements to my equity allocations. While they often generate higher yields than standard equities, these areas can also exhibit significantly less volatility than equities.

During periods when equity markets experience a meaningful decline, I often view these high-income exposures as “drier powder.” They provide a source of capital that can be reallocated to increase equity exposure when equity prices become more attractive. In the current environment, these assets are performing as I expect. While valuations in credit, dividend stocks, and closed-end funds appear somewhat elevated, they have not reached levels that would warrant a move to cash or other low-return defensive assets.

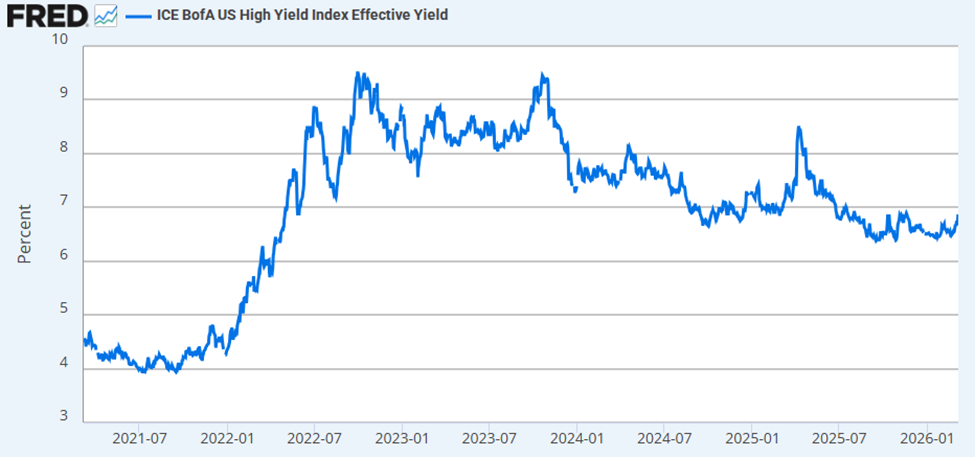

To assess the attractiveness of the high-income space, I frequently use high-yield spreads as a proxy for valuation. Broadly speaking, the wider the spread, which is the difference between high-yield bond rates and safe-haven Treasury rates, the more attractive these high-yield bond assets become.

Currently, spreads are relatively tight. This indicates that investors aren’t demanding a massive premium for taking on credit risk. With that said, absolute yields for high-yield bonds remain in the 6.5% to 7.0% range. For me as a patient investor, this level of income is still quite compelling as a complement with stocks.

I’ll continue to favor high-income generating assets and strategies as long as they provide this meaningful income advantage without an undue increase in risk.

High Yield Effective Yield

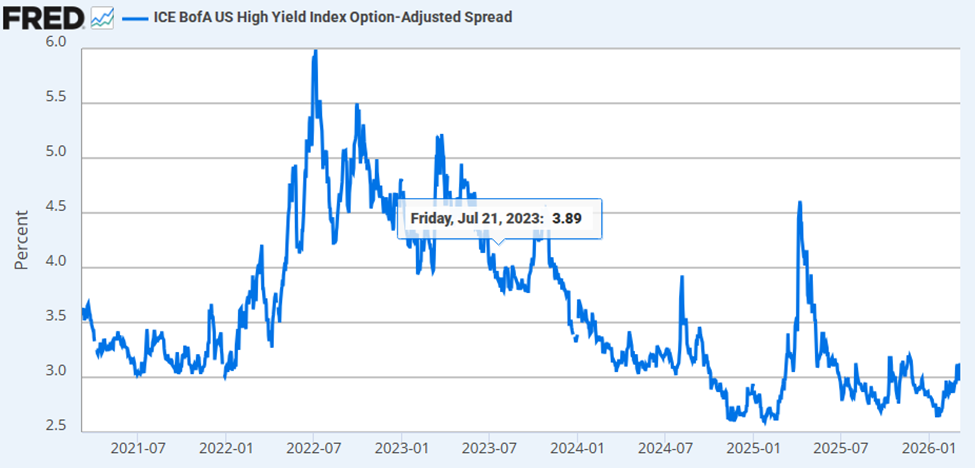

As the current data indicates, credit spreads remain notably tight. High-yield credit spreads have widened slightly in recent sessions, yet they still have significant room to expand further. When spreads are this narrow, it typically suggests that the market is pricing in a very optimistic economic outlook with little room for error. Conversely, if economic data weakens or if geopolitical tensions escalate further. credit-sensitive bond spreads could widen and the bonds could face price declines.

High Yield Bond Spreads

High-income generating assets and strategies have retreated from their recent peaks, yet this minor correction is not yet sufficient for me to become extremely aggressive. We have yet to see the kind of capitulation or fire sale pricing that typically marks an aggressive buying opportunity.

Despite the lack of extreme valuation discounts across high income-generating assets, I remain moderately bullish when these assets are viewed relative to the broader equity markets. U.S. equities continue to trade at extended valuations that leave little room for error, especially as geopolitical tensions persist.

Since my view of the income-to-volatility ratio remains favorable here, I prefer to maintain a healthy overweight position in these income-generating areas. This allows me to capture returns through income generation even if the price appreciation of the underlying indices remains stagnant or experiences a deeper correction.

COMMODITIES

I’ve shifted a bit of a mixed outlook on commodities.

Due to the significant rise in energy due to the Iran conflict, I have become moderately bearish on oil. With the persistent rally gold prices that started last year, I am somewhat fundamentally bearish on gold but technically slightly bullish.

Oil and gold prices have rallied into potentially overextended territory, and while supply shocks are real, the risk of a sharp mean reversion remains high if diplomatic tensions in Iran ease from these elevated levels.

Gold

I remain slightly bullish on gold but purely driven by market technicals rather than traditional fundamentals. Gold continues to trade above both its 50-day and 200-day moving averages, which is a classic bullish signal for momentum investors. As of March 10, 2026, spot gold is trading near $5,180, well above its 200-day moving average. As long as the technical price trends remain positive, I remain slightly bullish on gold.

I still don’t personally hold a strong fundamental view on gold. Historically, it has struggled to consistently act as a reliable hedge against any single economic metric. Large-scale central bank purchasing, which continues to be a major theme, is often driven by strategic reserve diversification rather than price sensitivity to supply and demand dynamics. These non-commercial buyers can keep prices elevated regardless of traditional valuation models.

The U.S. dollar has recently rallied from its lows, which has begun to exert some downward pressure on gold prices. Since gold is priced in dollars, a stronger dollar typically makes the metal more expensive for international buyers. If the conflict in Iran reaches a swift resolution, the fundamental pressure on the U.S. dollar could resume as “safe-haven” demand fades. If gold maintains its negative correlation with the dollar, we could see the precious metal continue to grind higher even as oil prices potentially weaken.

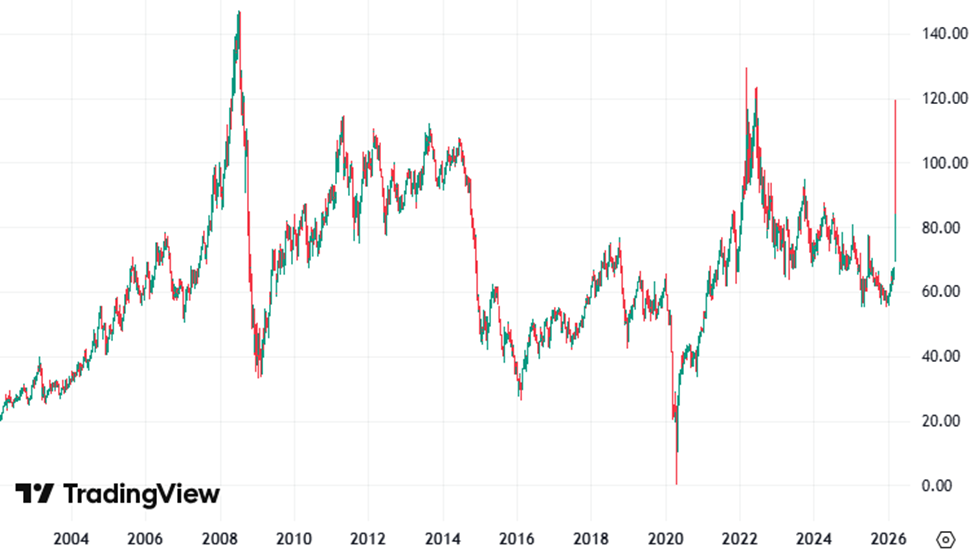

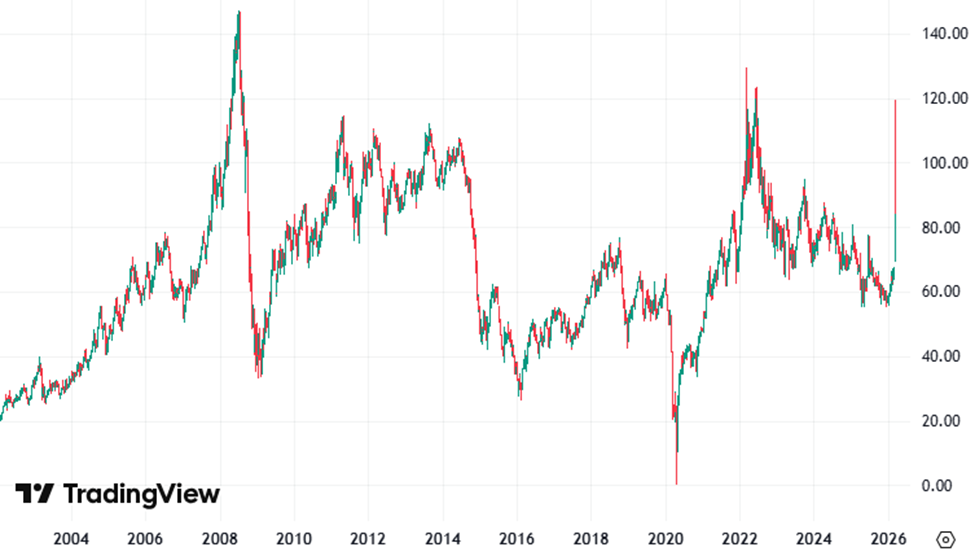

WTI Crude Oil

In my last Outlook & Positioning piece back in December, I was slightly bullish on WTI Crude Oil when it was trading in the mid-$50s. That has greatly shifted and I am now moderately bearish on WTI Crude Oil following its recent spike higher.

Oil prices experienced a violent rally higher following the U.S. and Israeli military strikes on Iran. In late-night trading on Sunday, March 8, 2026, WTI Crude Oil futures surged over 20%, briefly touching a peak of just under $120per barrel. This level is highly significant as it mirrors the major resistance point seen during the 2022 energy crisis. As expected, the commodity struggled to maintain momentum above the $110 to $120 range and has since pulled back to approximately $90 per barrel as of March 10, 2026.

WTI Crude Oil

I had indicated to my institutional clients that $120 per barrel could occur as it was a prior resistance point in 2022. Historically, WTI Crude Oil tends to trade within a core range of $55 to $90 per barrel. For me, when prices exceed the $90 threshold, the risk-to-reward profile shifts unfavorably for long positions, so I’d become increasingly bearish. While I was slightly bullish on oil in my previous outlook, the recent breach of the $90 to $120 zone has moved me into a moderately bearish stance. If prices were to test the $120 resistance level again, my bearish conviction would only increase.

The global economy is poorly positioned to absorb sustained triple-digit oil prices, and I think that global production could be ramped up and strategic petroleum reserves could be released to stabilize the market if necessary. If the Iranian conflict reaches a resolution within the next month or two, particularly one that reduces long-term geopolitical risk, oil could rapidly descend back toward the lower end of the $55 to $90 range.

Given these factors, I am moderately bearish on WTI Crude Oil at this time and was even more strongly so when oil reached $120 per barrel. If prices continue to fall, I would reduce my bearishness at that time.

CONSERVATIVE ASSETS

Conservative assets continue to generate attractive income for more risk-averse investors. My current preference is to remain diversified across multiple bond sectors with a focus on investment-grade bonds. Higher quality bonds can provide a necessary layer of protection and predictable cash flow in a volatile market.

To gain exposure to bonds across sectors, credit quality and duration, I continue to favor allocating to active bond managers that have the breadth, depth and experience to navigate the global bond markets.

As previously discussed, high-yield credit spreads are still quite tight. Historically, when spreads are narrow, there is a heightened risk that they will widen if market volatility continues to rise, leading to price declines in riskier debt. There would be no reason for me to take on additional credit risk in a conservative allocation at these levels. I would much rather remain patient and wait for a clear opportunity to increase exposure to credit-sensitive bonds when the risk-to-reward ratio becomes more favorable. The markets simply have not reached that point yet.

Municipal bond investors may continue to find unique opportunities in the current environment. Unlike some of their taxable counterparts, municipal bond yields have not compressed to the same degree, allowing them to offer relatively attractive tax-equivalent yields.

The U.S. yield curve has remained relatively stable, with the 10-year Treasury yield continuing to trade within a narrow range. Depending on the market environment, I would consider increasing portfolio duration if the 10-year Treasury yield climbs above 4.5%, as this provides a more attractive entry point for locking in long-term rates. I would probably look to reduce duration if yields fall below 3.5%, where the risk of a reversal could outweigh the potential for further price appreciation.

10 Year U.S. Treasury Yield

The fiscal landscape is becoming increasingly complex. With the added expenditures associated with the conflict in Iran, U.S. debt levels are not expected to decline in the foreseeable future. This persistent supply of government debt could put upward pressure on the longer end of the yield curve.

We must also consider the potential for an economic slowdown. If the conflict in Iran is prolonged and begins to significantly hamper global growth, the U.S. economy could weaken. In this scenario, the Federal Reserve might feel compelled to reduce the federal funds rate. While the fed funds rate does not have a direct mathematical link to intermediate or long-term yields, a shift toward a more accommodative monetary policy could exert downward pressure on the entire curve. This could result in Treasury prices rallying from current levels.

With my preference to remain diversified across bond sectors, credit quality and duration through the utilization of active bond managers, I think I can maintain some stability in my bond allocation relative to my higher volatility exposure to equities. By blending government bonds for potential liquidity and safety with securitized assets for incremental yield, investors can create a more resilient conservative sleeve. This multi-sector approach allows me to capture the carry provided by higher-yielding cash flows while ensuring the portfolio remains anchored if broader risk assets take another leg lower.

U.S. GOVERNMENT BONDS

I remain slightly bullish on U.S. government bonds.

U.S. government bonds can still act as a short-term high quality asset in a “flight-to-quality” scenario. I think maintaining exposure to government bonds is a prudent strategy to consider for conservative investors seeking a buffer against equity market volatility.

My personal preference remains to be diversified across bond sectors, including investment grade securitized assets (MBS, CMBS, ABS, etc.) and corporate bonds.

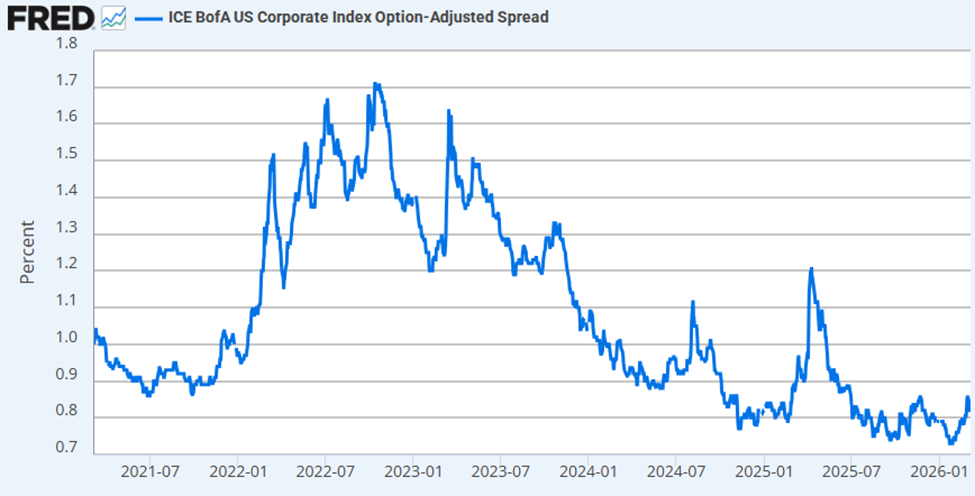

U.S. INVESTMENT GRADE CREDIT

I remain slightly bullish on U.S. investment grade securitized assets and corporate bonds.

Credit spreads across investment grade securitized assets and corporate bonds remain tight, so I don’t have any reason to get overly aggressive on these areas relative to the “safe-haven” assets of U.S. Treasuries or the implicit guarantee of agency mortgage-backed securities (MBS).

Even though credit spreads have widened a little bit following the start of the Iranian conflict, spreads aren’t even close to being attractive for me to add risk aggressively to an allocation reserved for conservative assets.

U.S. Investment Grade Corporate Bond Spreads

OTHER

I use this section to talk about other potential strategies, generally whether or not hedges are needed on asset classes.

I remain slightly bullish on non-traditional investment hedging strategies at this time.

While market volatility has certainly picked up, it remains well within the normal parameters we expect to see in any given year. Rather than pivoting to overly complex or opaque hedging instruments, I continue to favor traditional asset classes, specifically credit-sensitive bonds that are currently generating attractive absolute income yields.

I think this recent bout of volatility is healthy. It serves to clear out some of the speculative excess we saw in 2025 and early 2026 and allows the market to reset its valuation floor. Unless we see oil prices spike and sustain levels significantly higher and threaten to break the broader economy, I don’t think that U.S. economic or corporate fundamentals will be dramatically compromised by the ongoing conflict in Iran.

My investment strategy hasn’t changed, I’ll remain patient and let the markets come to me. If global equity and credit markets decline further to hit levels that are attractive to me, I’ll consider adding risk exposure. If not, I’ll continue to wait and allow my income-generating assets continue to generate income, and I’ll tactically rebalance when and where appropriate.

Just keeping it simple.

Eric Kulwicki, CFA®, CFP®, brings 20+ years of experience, currently serving as an independent investment consultant, portfolio manager, and wealth advisor for institutional and retail clients. On KulwickiInsights.com, Eric shares his timely perspectives on financial markets, investment strategies, and other financial topics. He also offers online investment education courses for beginner and intermediate investors, and coaching sessions for DIY investors seeking professional guidance.